Article content

(Bloomberg) — Shares in Asia fell Monday as investors look ahead to US inflation data due Tuesday that is expected to show a further slowing in core prices.

Equities in Australia, South Korea and Japan all declined. The Topix index of Japanese equities faced its biggest one-day drop since October, weighed down by the tech sector which lost almost 3%. The tech-heavy Nikkei 225 index also fell with other Asian chip and AI-related stocks after Nvidia Corp. slipped 5.6% Friday.

Advertisement 2

Article content

Article content

Hong Kong equity futures went against the broader trend to trade higher, helped along by the first rise in consumer prices since August. The 0.7% increase in February CPI exceeded consensus estimates and is welcome news for investors worried about deflation in the world’s second largest economy.

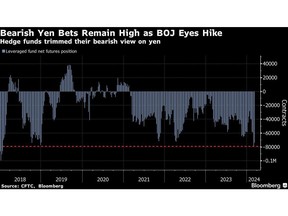

Economic growth in Japan expanded in the fourth-quarter, supporting expectations that the Bank of Japan will raise interest rates for the first time since 2007 as soon as this month. Declines for Japanese shares partly reflected the stronger yen, which typically acts as a headwind for the country’s equities.

The currency was firmer against the greenback in early trading Monday, extending its 2% rally last week against the US currency — its best weekly gain since July. Japanese bond yields gained on a report stating that the BOJ is considering scrapping its yield curve control program.

“Perhaps, Japan is finally coming out of this deflationary vortex and that could have profound implications on Japanese assets,” said Paresh Upadhyaya, director of fixed income and currency strategy at Amundi Asset Management, explaining that this will be supportive for the yen through repatriation flows, mainly going into stocks.

Top Stories

Article content

Advertisement 3

Article content

Tuesday’s US consumer price index figures will dominate the economic data reports this week. The core prices gauge is seen rising 0.3% in February from a month earlier, and 3.7% on a year-over-year basis — which would be the smallest annual rise since April 2021.

Further moderation in US prices would support the disinflation narrative that broadly remains in tact, despite a pullback in the number of Federal Reserve rate cuts expected this year. Swaps pricing shows three cuts are anticipated in 2024, down from six at the start of the year.

Last week’s US jobs data did little to change that outlook. The jobless rate touched a two-year high, even as the number of new jobs added exceeded estimates. The mixed signal points to a slowly cooling labor market that, for now, supports expectations for a soft landing in the US economy.

The jobs report “didn’t necessarily amount to an ‘all-clear’ signal for the Fed, but there also didn’t appear to be anything in it that would derail its plan to cut rates,” said Chris Larkin at E*Trade from Morgan Stanley.

Yields in Australia were largely flat Monday, reflecting the steady trading in Treasuries in Asia. An index of the dollar was weaker after falling 1% last week — the worst weekly showing since December.

Advertisement 4

Article content

Contracts for US stocks slipped Monday, extending the downbeat end to the week in the US, where both the S&P 500 and the Nasdaq 100 fell. The pullback in US equities on Friday reflected a decline for most of the so-called Magnificent Seven stocks that have powered the US market to fresh highs this year.

In commodities, oil held a loss Monday ahead of reports from OPEC and the IEA this week that may provide clues on the demand outlook. Gold edged higher, extending Friday’s almost 1% gain. Bitcoin fell below $68,000.

Key Events This Week:

- CPI reports for Argentina, Brazil, Germany, India, US, Tuesday

- UK jobless claims, unemployment, Tuesday

- Japan PPI, Tuesday

- India industrial production, Tuesday

- Mexico international reserves, industrial production, Tuesday

- Philippines trade, Tuesday

- Turkey industrial production, current account, Tuesday

- EU finance ministers meet in Brussels, Tuesday

- ECB Governing Council Member Robert Holzmann speaks, Tuesday

- Eurozone, UK industrial production, Wednesday

- India trade, Wednesday

- South Korea jobless rate, Wednesday

- ECB Governing Council member Yannis Stournaras speaks, Wednesday

- Swedish Riksbank First Deputy Governor and Deputy Governor speak, Wednesday

- Saudi Arabia, Spain CPI, Thursday

- US PPI, retail sales, initial jobless claims, business inventories, Thursday

- Australia Treasurer Jim Chalmers delivers pre-budget address, Thursday

- Canada housing starts, Friday

- China property prices, Friday

- France, Italy, Poland CPI, Friday

- Indonesia trade, Friday

- Japan tertiary index, Friday

- New Zealand PMI, Friday

- Philippines overseas remittances, Friday

- Sri Lanka GDP

- US industrial production, University of Michigan consumer sentiment, Empire Manufacturing, Friday

- Japan’s largest union federation announces results of annual wage negotiations, Friday

Advertisement 5

Article content

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 9:55 a.m. Tokyo time

- Hang Seng futures rose 0.2%

- Nikkei 225 futures (OSE) fell 2.6%

- Japan’s Topix fell 2%

- Australia’s S&P/ASX 200 fell 1.4%

- Euro Stoxx 50 futures fell 0.5%

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%

- The euro was little changed at $1.0944

- The Japanese yen rose 0.2% to 146.72 per dollar

- The offshore yuan was little changed at 7.1957 per dollar

- The Australian dollar was unchanged at $0.6624

Cryptocurrencies

- Bitcoin fell 2.1% to $67,946.91

- Ether fell 2.3% to $3,818.2

Bonds

- The yield on 10-year Treasuries was little changed at 4.07%

- Japan’s 10-year yield advanced 3.5 basis points to 0.765%

- Australia’s 10-year yield was little changed at 3.97%

Commodities

- West Texas Intermediate crude fell 0.5% to $77.62 a barrel

- Spot gold rose 0.4% to $2,187.49 an ounce

This story was produced with the assistance of Bloomberg Automation.

Article content